I. What is a Business Line of Credit?

A business line of credit is a flexible financing option that provides a revolving credit limit to businesses. It allows businesses to borrow money up to a certain limit and repay it over time. Unlike a traditional loan, businesses only pay interest on the amount they use. This provides businesses with ongoing access to funds for managing cash flow, purchasing inventory, and covering other short-term expenses. To understand more about business lines of credit, click here.

II. Importance of Interest Only Payment Calculator

Benefits and usefulness of using an interest only payment calculator for a business line of credit

When it comes to managing your business line of credit, utilizing an interest only payment calculator can be highly beneficial. Here are some of the key benefits and reasons why using an interest only payment calculator is important:

Accurate calculations: An interest only payment calculator can provide you with precise calculations of your interest payments, allowing you to plan and budget accordingly.

Easy comparison: By entering different interest rates or loan terms into the calculator, you can easily compare the impact on your payments and make informed decisions about your business line of credit.

Financial planning: Using an interest only payment calculator enables you to plan your cash flow and evaluate the affordability of the interest-only payments on your business line of credit.

Understanding repayment options: With an interest only payment calculator, you can determine the potential savings and costs associated with different repayment options, helping you find the most suitable and cost-effective solution for your business.

Identifying potential risks: By being able to calculate the interest payments accurately, you can identify potential risks and determine the impact they may have on your financial stability.

Flexible scenarios: An interest only payment calculator allows you to explore different scenarios, such as making additional payments or modifying the interest rate, helping you optimize your financial strategy for your business line of credit.

Using an interest only payment calculator can provide you with valuable insights and help you make informed decisions when managing your business line of credit. It is a useful tool that can contribute to the financial success and stability of your business.

III. Factors to Consider When Choosing a Business Line of Credit

Key considerations in selecting a business line of credit

When deciding on a business line of credit, there are several important factors to consider. These include:

- Interest rates: Compare the interest rates offered by different lenders to ensure you're getting the best deal.

- Credit limit: Determine the maximum amount you can borrow with the line of credit.

- Repayment terms: Understand the repayment terms, including interest-only payment options.

- Fees and charges: Consider any additional fees or charges associated with the business line of credit.

- Flexibility: Look for a line of credit that offers flexibility in terms of borrowing and repayment.

- Lender reputation: Research the reputation and reliability of the lender before making a decision.

By carefully considering these factors, you can choose a business line of credit that meets your financial needs and goals.

IV. Introduction to Interest Only Payment Calculator

Explanation of what an interest only payment calculator is and how it functions

Are you considering a business line of credit? An interest only payment calculator can be a useful tool to help you estimate and plan your monthly payments. This calculator allows you to input details such as the loan amount, interest rate, and loan term to calculate the monthly interest-only payment. It is a helpful tool for understanding and managing your financial obligations.

V. How to Use the Interest Only Payment Calculator

Using the interest only payment calculator is a straightforward process. Here is a step-by-step guide on how to utilize the calculator to determine interest-only payment amounts:

- Input the loan amount: Enter the total amount of the loan you are considering.

- Enter the interest rate: Input the interest rate for the loan.

- Select the loan term: Choose the duration of the loan in months or years.

- Click calculate: Press the calculate button, and the calculator will display the interest-only payment amount.

With this tool, you can easily calculate interest-only payments for your business line of credit and plan your financial strategy accordingly.

:max_bytes(150000):strip_icc()/loan-payment-calculations-315564-70a2f63dbd624881b63ec5392209c9a6.gif)

VI. Example Calculation

Demonstration of a sample calculation using the interest only payment calculator

To better understand how an interest-only payment calculator works, let's consider an example. Suppose you have taken out a business line of credit with a principal amount of $100,000 and an annual interest rate of 8%. You want to calculate the monthly interest-only payment for the first year.

Using the interest only payment calculator, you would input the principal amount ($100,000) and the annual interest rate (8%). The calculator would then provide you with the monthly interest-only payment, which in this case would be $666.67.

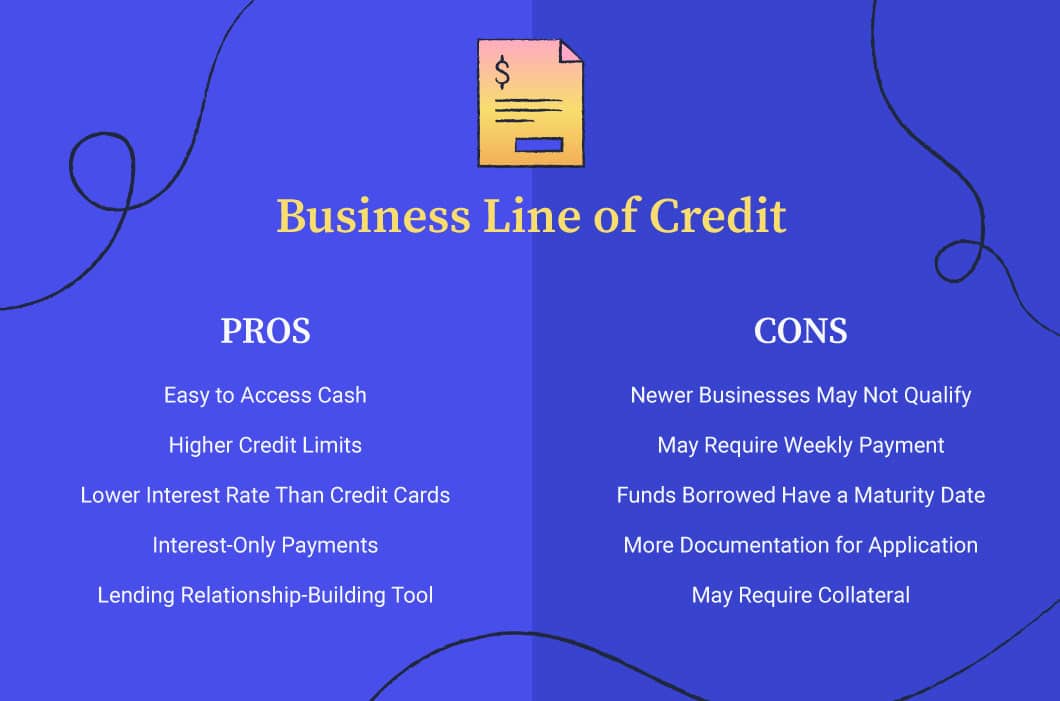

VII. Advantages of Interest Only Payments

Benefits and advantages of interest only payment for a business line of credit

Interest only payments can offer several advantages for businesses utilizing a line of credit. These advantages include:

Lower Monthly Payments: With interest only payments, businesses only need to pay the interest accrued each month, resulting in lower monthly payments compared to principal and interest payments.

Improved Cash Flow: Lower monthly payments free up cash flow for businesses, allowing them to allocate resources to other areas of operations or investment opportunities.

Flexibility: Interest only payments provide businesses with greater flexibility in managing their finances. They have the option to pay only the interest during periods of lower cash flow and allocate more funds towards principal payments during periods of higher cash flow.

Initial Cost Savings: Businesses may save money on initial costs since they are not required to pay off the principal balance immediately. This can be particularly beneficial for start-ups or businesses with fluctuating cash flows.

Management of Seasonal Cash Flow Variations: For businesses that experience seasonal fluctuations in cash flow, interest only payments can help them better manage their financial obligations during slower periods.

It's important to note that while interest only payments offer certain advantages, businesses need to carefully consider their long-term financial goals and the overall cost of interest over the life of the loan. Consulting with a financial advisor or accountant can provide valuable insights into the best payment structure for a business line of credit.

VIII. Limitations and Risks of Interest Only Payments

Potential drawbacks and risks associated with making interest only payments on a business line of credit

While interest-only payments on a business line of credit can provide flexibility and lower initial payments, there are several potential limitations and risks to consider:

Increased overall cost: By only paying interest, the principal balance remains untouched, which means the total cost of borrowing over time may be higher.

Prolonged repayment period: Without paying down the principal, the repayment period for the line of credit may be extended, leading to longer-term debt.

Variable interest rates: If the line of credit has a variable interest rate, the cost of interest payments may increase over time, making it harder to predict and plan for future expenses.

Unforeseen financial challenges: If your business experiences financial difficulties or cash flow problems, relying solely on interest-only payments may not provide sufficient flexibility to address these challenges.

Reduced credit availability: By only paying interest, you may not be able to access additional credit or increase your credit limit, limiting your ability to expand or invest in your business.

It is important to carefully assess the limitations and risks associated with interest-only payments and consider the financial stability and goals of your business before choosing this repayment option.

:max_bytes(150000):strip_icc()/interestcoverageratio-f7e7cdf96d4b4063a63d258ff5d775a8.jpg)

IX. Conclusion

Summary and key takeaways regarding using an interest only payment calculator for a business line of credit.

In conclusion, using an interest only payment calculator can be a valuable tool for businesses looking to manage their cash flow and understand the cost of borrowing. Key takeaways include:

- Interest only payment calculators provide businesses with the ability to estimate their monthly interest payments on a business line of credit.

- It is important to understand the terms and conditions of your line of credit, including the interest rate, repayment period, and any potential fees.

- By inputting the necessary information into the interest only payment calculator, businesses can get a clear understanding of the financial impact of their line of credit.

- Calculating interest only payments can help businesses make informed decisions about their borrowing needs and evaluate the affordability of the loan.

Remember, an interest only payment calculator is just one tool in the financial management toolbox. It is always recommended to consult with a financial advisor or lender for personalized advice and guidance based on your specific business needs and circumstances.

This comment has been removed by the author.

ReplyDelete